> For the complete documentation index, see [llms.txt](https://gitbook-docs.coinmetrics.io/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://gitbook-docs.coinmetrics.io/tutorials-and-examples/tutorials/walkthrough_community.md).

# Python API Client Walkthrough

## Python API Client Walkthrough

*Last Updated: Version `2024.08.20`*

This notebook demonstrates basic functionality offered by the Coin Metrics Python API Client using Coin Metrics Community Data.

Coin Metrics offers a vast assortment of data for hundreds of cryptoassets. The Python API Client allows for easy access to this data using Python without needing to create your own wrappers using `requests` and other such libraries.

### Prerequisites

First, Python must be installed. Download and install from [python.org](https://www.python.org/downloads/). The Coin Metrics API Client is best used with Python 3.8 or later.

Then, install the Python API Client:

`pip install coinmetrics-api-client`

Some of the optional libraries such as pandas, numpy, and seaborn are used in the notebook to make the examples more interactive. These libraries are not required to use the Coin Metrics API Client.

You are now ready to run the code in the rest of the notebook.

### Resources

To understand the data that Coin Metrics offers, feel free to peruse the resources below.

* The [Coin Metrics API v4](https://docs.coinmetrics.io/api/v4) website contains the full set of endpoints and data offered by Coin Metrics.

* The [Coin Metrics Product Documentation](https://docs.coinmetrics.io/) gives detailed, conceptual explanations of the data that Coin Metrics offers.

* The [API Spec](https://docs.coinmetrics.io/python-api-client/reference) contains a full list of functions.

* The [Coverage Tool](https://coverage.coinmetrics.io/) shows what assets, metrics, and other data types are covered.

### Setup

```python

from os import environ

import sys

import pandas as pd

import numpy as np

import seaborn as sns

import logging

from datetime import date, datetime, timedelta

from coinmetrics.api_client import CoinMetricsClient

import matplotlib.pyplot as plt

# %matplotlib inline

```

```python

logging.basicConfig(

format='%(asctime)s %(levelname)-8s %(message)s',

level=logging.INFO,

datefmt='%Y-%m-%d %H:%M:%S'

)

```

```python

# We recommend privately storing your API key in your local environment.

# Uncomment below if you have an API Key. Otherwise we will use Community data.

# try:

# api_key = environ["CM_API_KEY"]

# logging.info("Using API key found in environment")

# except KeyError:

# api_key = ""

# logging.info("API key not found. Using community client")

client = CoinMetricsClient()

# client = CoinMetricsClient(api_key)

```

```python

assets = ['btc', 'eth']

metrics = ['ReferenceRateUSD', 'CapMrktEstUSD']

start_time = datetime(year=2024, month=9, day=1)

end_time = datetime(year=2024, month=9, day=30)

asset_mapping = {i: assets[i] for i in range(len(assets))}

```

```

{0: 'btc', 1: 'eth'}

```

### Catalogs

The Coin Metrics API contains two types of catalog endpoints (Python client functions in paranthesis): the `catalog` (`catalog_*_v2`) and `catalog-all` (`catalog_full_*_v2`).

The `catalog` endpoint displays the set of data available to your API key. The `catalog-all` endpoint displays the full set of data for our dataset.

```python

asset_metrics_catalog = client.catalog_asset_metrics_v2(assets=assets).to_list()

full_asset_metrics_catalog = client.catalog_full_asset_metrics_v2(assets=assets).to_list()

```

Catalog objects return a list of dictionaries. For `catalog_asset_metrics_v2`, each element of the list is an asset, while each dictionary is a set of metadata for that specific asset.

```python

print(f"Asset Metrics Catalog metadata includes: {list(asset_metrics_catalog[0].keys())}")

for i in asset_mapping:

print(f"Asset {asset_mapping[i]} has {len(asset_metrics_catalog[i]['metrics'])} metrics in catalog.")

print(f"Asset {asset_mapping[i]} has {len(full_asset_metrics_catalog[i]['metrics'])} metrics in catalog-all.")

```

```

Asset Metrics Catalog metadata includes: ['asset', 'metrics']

Asset btc has 147 metrics in catalog.

Asset btc has 696 metrics in catalog-all.

Asset eth has 146 metrics in catalog.

Asset eth has 699 metrics in catalog-all.

```

```

Asset Metrics Catalog metadata includes: ['asset', 'metrics']

Asset btc has 147 metrics in catalog.

Asset btc has 513 metrics in catalog-all.

Asset eth has 146 metrics in catalog.

Asset eth has 500 metrics in catalog-all.

```

For more details on what metrics are covered, see [Coverage](https://coverage.coinmetrics.io/asset-metrics-v2)

### Getting Timeseries Data

Next, we will pull timeseries data. Typically there are two types of timeseries data that you can pull: raw observations such as trades and aggregated metrics. We will explore these two below.

#### Asset Metrics

First, we will use the [`asset-metrics`](https://docs.coinmetrics.io/api/v4/#tag/Timeseries/operation/getTimeseriesAssetMetrics) endpoint to get metrics for BTC and ETH.

```python

btc_metrics = [m['metric'] for m in asset_metrics_catalog[0]['metrics']]

eth_metrics = [m['metric'] for m in asset_metrics_catalog[1]['metrics']]

```

You can bound your query by time like below:

```python

df_asset_metrics = client.get_asset_metrics(

assets=assets,

metrics=metrics,

start_time=start_time,

end_time=end_time

).to_dataframe()

```

```python

df_asset_metrics.head()

```

| | asset | time | CapMrktEstUSD | ReferenceRateUSD |

| - | ----- | ------------------------- | -------------------- | ---------------- |

| 0 | btc | 2024-09-01 00:00:00+00:00 | 1132518348250.186279 | 58959.926273 |

| 1 | btc | 2024-09-02 00:00:00+00:00 | 1168286956855.852539 | 57349.080718 |

| 2 | btc | 2024-09-03 00:00:00+00:00 | 1138274882375.744873 | 59159.023888 |

| 3 | btc | 2024-09-04 00:00:00+00:00 | 1146114653782.878418 | 57637.775444 |

| 4 | btc | 2024-09-05 00:00:00+00:00 | 1108213762229.152832 | 58033.39897 |

| | asset | time | CapMrktEstUSD | ReferenceRateUSD |

| - | ----- | ------------------------- | -------------------- | ---------------- |

| 0 | btc | 2024-08-15 00:00:00+00:00 | 1137894996787.05249 | 58840.64668 |

| 1 | btc | 2024-08-16 00:00:00+00:00 | 1163252605521.227783 | 57644.187688 |

| 2 | btc | 2024-08-17 00:00:00+00:00 | 1172900035803.550781 | 58927.276509 |

| 3 | btc | 2024-08-18 00:00:00+00:00 | 1160659435495.434814 | 59414.674335 |

| 4 | btc | 2024-08-19 00:00:00+00:00 | 1172894781992.733887 | 58793.206146 |

```python

df_asset_metrics.loc[df_asset_metrics.asset=='btc'].plot(x='time', y='ReferenceRateUSD')

```

Coin Metrics supports several metrics for various data types such as exchanges, markets, and asset-pairs.

You can also bound your queries by using the `limit` parameter.

```python

df_asset_metrics_limit = client.get_asset_metrics(

assets=assets,

metrics=btc_metrics[:5],

start_time=start_time,

end_time=end_time,

limit_per_asset=2

).to_dataframe()

```

```python

df_asset_metrics_limit

```

| | asset | time | AdrActCnt | AdrBal1in100KCnt | AdrBal1in100MCnt | AdrBal1in10BCnt | AdrBal1in10KCnt |

| - | ----- | ------------------------- | --------- | ---------------- | ---------------- | --------------- | --------------- |

| 0 | btc | 2024-09-01 00:00:00+00:00 | 660770 | 9283 | 3046587 | 20365534 | 973 |

| 1 | btc | 2024-09-02 00:00:00+00:00 | 717673 | 9284 | 3046904 | 20359814 | 972 |

| 2 | eth | 2024-09-01 00:00:00+00:00 | 548611 | 6907 | 1836310 | 27996184 | 1221 |

| 3 | eth | 2024-09-02 00:00:00+00:00 | 488354 | 6902 | 1836617 | 28008369 | 1218 |

| | asset | time | AdrActCnt | AdrBal1in100KCnt | AdrBal1in100MCnt | AdrBal1in10BCnt | AdrBal1in10KCnt |

| - | ----- | ------------------------- | --------- | ---------------- | ---------------- | --------------- | --------------- |

| 0 | btc | 2024-08-15 00:00:00+00:00 | 715632 | 9229 | 3054724 | 20292616 | 973 |

| 1 | btc | 2024-08-16 00:00:00+00:00 | 700335 | 9231 | 3055010 | 20300505 | 977 |

| 2 | eth | 2024-08-15 00:00:00+00:00 | 603353 | 6862 | 1837926 | 27972812 | 1226 |

| 3 | eth | 2024-08-16 00:00:00+00:00 | 541263 | 6871 | 1837366 | 27962507 | 1223 |

#### Market Observations

The other common timeseries data type that you will encounter are individual observations.

First, we will need to familiarize ourselves with the market convention which we can find on faqs. You can see a full list of markets by using the `reference-data` endpoint.

```python

df_coinbase_btc_markets = client.reference_data_markets(asset='btc', exchange='coinbase').to_dataframe()

```

```python

df_coinbase_btc_markets.head()

```

| | market | exchange | base | quote | pair | symbol | type | size\_asset | margin\_asset | strike | ... | order\_price\_increment | order\_price\_min | order\_price\_max | order\_size\_min | order\_taker\_fee | order\_maker\_fee | margin\_trading\_enabled | experimental | base\_native | quote\_native |

| - | ----------------------- | -------- | ----- | ----- | --------- | --------- | ---- | ----------- | ------------- | ------ | --- | ----------------------- | ----------------- | ----------------- | ---------------- | ----------------- | ----------------- | ------------------------ | ------------ | ------------ | ------------- |

| 0 | coinbase-1inch-btc-spot | coinbase | 1inch | btc | 1inch-btc | 1INCH-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 1 | coinbase-aave-btc-spot | coinbase | aave | btc | aave-btc | AAVE-BTC | spot | \ | \ | \ | ... | 0.000001 | 0.000001 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 2 | coinbase-ada-btc-spot | coinbase | ada | btc | ada-btc | ADA-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 3 | coinbase-algo-btc-spot | coinbase | algo | btc | algo-btc | ALGO-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 4 | coinbase-ankr-btc-spot | coinbase | ankr | btc | ankr-btc | ANKR-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

5 rows × 39 columns

| | market | exchange | base | quote | pair | symbol | type | size\_asset | margin\_asset | strike | ... | order\_amount\_min | order\_amount\_max | order\_price\_increment | order\_price\_min | order\_price\_max | order\_size\_min | order\_taker\_fee | order\_maker\_fee | margin\_trading\_enabled | experimental |

| - | ----------------------- | -------- | ----- | ----- | --------- | --------- | ---- | ----------- | ------------- | ------ | --- | ------------------ | ------------------ | ----------------------- | ----------------- | ----------------- | ---------------- | ----------------- | ----------------- | ------------------------ | ------------ |

| 0 | coinbase-1inch-btc-spot | coinbase | 1inch | btc | 1inch-btc | 1INCH-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

| 1 | coinbase-aave-btc-spot | coinbase | aave | btc | aave-btc | AAVE-BTC | spot | \ | \ | \ | ... | \ | \ | 0.000001 | 0.000001 | \ | 0.000016 | \ | \ | False | \ |

| 2 | coinbase-ada-btc-spot | coinbase | ada | btc | ada-btc | ADA-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

| 3 | coinbase-algo-btc-spot | coinbase | algo | btc | algo-btc | ALGO-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

| 4 | coinbase-ankr-btc-spot | coinbase | ankr | btc | ankr-btc | ANKR-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

5 rows × 37 columns

We can then pass these markets onto the `timeseries/market-*` endpoints. Below is an example of how to pull individual market trades.

```python

df_coinbase_btc_trades = client.get_market_trades(

markets=["coinbase-btc-usd-spot"],

start_time=datetime.now()-timedelta(seconds=60),

end_time=datetime.now(),

).to_dataframe()

```

```python

df_coinbase_btc_trades.head()

```

| | market | time | coin\_metrics\_id | amount | price | database\_time | side |

| - | --------------------- | -------------------------------- | ----------------- | -------- | -------- | -------------------------------- | ---- |

| 0 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966854 | 0.000004 | 68353.27 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 1 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966855 | 0.000012 | 68353.27 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 2 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966856 | 0.002187 | 68354.37 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 3 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966857 | 0.002523 | 68354.38 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 4 | coinbase-btc-usd-spot | 2024-10-25 15:22:45.078614+00:00 | 705966858 | 0.001043 | 68353.27 | 2024-10-25 15:22:45.721609+00:00 | buy |

| | market | time | coin\_metrics\_id | amount | price | database\_time | side |

| - | --------------------- | -------------------------------- | ----------------- | -------- | -------- | -------------------------------- | ---- |

| 0 | coinbase-btc-usd-spot | 2024-09-13 16:55:02.663733+00:00 | 691698441 | 0.008 | 59491.6 | 2024-09-13 16:55:03.253369+00:00 | sell |

| 1 | coinbase-btc-usd-spot | 2024-09-13 16:55:02.670644+00:00 | 691698442 | 0.008 | 59491.61 | 2024-09-13 16:55:03.253369+00:00 | buy |

| 2 | coinbase-btc-usd-spot | 2024-09-13 16:55:03.057923+00:00 | 691698443 | 0.001186 | 59491.61 | 2024-09-13 16:55:03.771512+00:00 | buy |

| 3 | coinbase-btc-usd-spot | 2024-09-13 16:55:03.143752+00:00 | 691698444 | 0.15742 | 59491.6 | 2024-09-13 16:55:03.771512+00:00 | sell |

| 4 | coinbase-btc-usd-spot | 2024-09-13 16:55:03.143816+00:00 | 691698445 | 0.076281 | 59491.6 | 2024-09-13 16:55:03.771512+00:00 | sell |

#### Examples from State of the Network

The Python API Client is often used for transforming data for [State of the Network](https://coinmetrics.substack.com/). Below are some examples of data transformations done to produce the data visualizations.

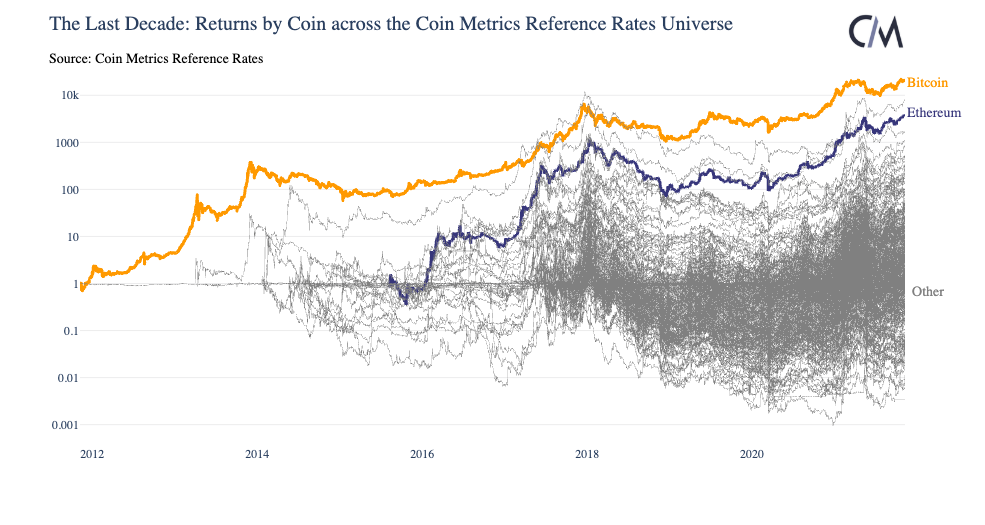

**Example 1: Get returns by coin in the CM reference rates universe over the last 10-years**

In [State of the Network #128](https://coinmetrics.substack.com/p/coin-metrics-state-of-the-network-53b), we looked at the returns for each asset dating back the last 10 years.

We can generate this data by weaving in the `catalog_asset_metrics_v2` and `get_asset_metrics` endpoint. The code snippets below demonstrate how to do this with a small list of assets.

```python

# Get all assets that have a reference rate

assets_refrate = client.catalog_asset_metrics_v2(metrics="ReferenceRateUSD")

# Get list of assets with daily ref rate

# uncomment the top line to look at *every* asset with reference rates

# asset_with_ref_rates = assets_refrate[0]["frequencies"][0]["assets"]

asset_with_ref_rates = ['btc', 'eth', 'bnb', 'ada', 'doge', 'xrp']

#Query API for prices, daily CM reference rates as dataframe

metrics = "ReferenceRateUSD"

frequency = "1d"

logging.info("Getting prices...")

df_prices = client.get_asset_metrics(

assets=asset_with_ref_rates,

metrics=metrics,

frequency=frequency,

start_time=start_time,

end_time=end_time

).to_dataframe()

# Assign datatypes

df_prices["time"] = pd.to_datetime(df_prices.time)

df_prices["ReferenceRateUSD"] = df_prices.ReferenceRateUSD.astype(float)

# Reshape dataset so assets are in columns, dates are the rows, and the values are prices

df_prices_pivot = df_prices.pivot(

index="time",

columns="asset",

values="ReferenceRateUSD"

)

# Index each asset's time series to 1

for col in df_prices_pivot.columns:

logging.info(f"Calculating Reference rate for {col}....")

# First price in time series

first_price = df_prices_pivot[df_prices_pivot[col].notnull()][col].iloc[0]

# Index time series

df_prices_pivot[col] = df_prices_pivot[col]/first_price

# Fill forward for Null values

df_prices_pivot[col] = df_prices_pivot[col].ffill()

```

```

2024-10-25 15:23:44 INFO Getting prices...

2024-10-25 15:23:45 INFO Calculating Reference rate for ada....

2024-10-25 15:23:45 INFO Calculating Reference rate for bnb....

2024-10-25 15:23:45 INFO Calculating Reference rate for btc....

2024-10-25 15:23:45 INFO Calculating Reference rate for doge....

2024-10-25 15:23:45 INFO Calculating Reference rate for eth....

2024-10-25 15:23:45 INFO Calculating Reference rate for xrp....

```

```

2024-09-13 16:56:10 INFO Getting prices...

2024-09-13 16:56:11 INFO Calculating Reference rate for ada....

2024-09-13 16:56:11 INFO Calculating Reference rate for bnb....

2024-09-13 16:56:11 INFO Calculating Reference rate for btc....

2024-09-13 16:56:11 INFO Calculating Reference rate for doge....

2024-09-13 16:56:11 INFO Calculating Reference rate for eth....

2024-09-13 16:56:11 INFO Calculating Reference rate for xrp....

```

```python

df_prices_pivot.tail()

```

| asset | ada | bnb | btc | doge | eth | xrp |

| ------------------------- | -------- | -------- | -------- | -------- | -------- | -------- |

| time | | | | | | |

| 2024-09-26 00:00:00+00:00 | 1.102137 | 1.100617 | 1.069534 | 1.070347 | 1.024427 | 1.030510 |

| 2024-09-27 00:00:00+00:00 | 1.162204 | 1.118540 | 1.103424 | 1.164025 | 1.046276 | 1.042040 |

| 2024-09-28 00:00:00+00:00 | 1.165724 | 1.141772 | 1.115465 | 1.222446 | 1.073526 | 1.040046 |

| 2024-09-29 00:00:00+00:00 | 1.158667 | 1.127693 | 1.115512 | 1.267128 | 1.064176 | 1.084632 |

| 2024-09-30 00:00:00+00:00 | 1.151477 | 1.119118 | 1.112921 | 1.232789 | 1.056856 | 1.133519 |

| asset | ada | bnb | btc | doge | eth | xrp |

| ------------------------- | -------- | -------- | -------- | -------- | -------- | -------- |

| time | | | | | | |

| 2024-09-09 00:00:00+00:00 | 1.008826 | 0.960197 | 0.932336 | 0.936040 | 0.862489 | 0.930312 |

| 2024-09-10 00:00:00+00:00 | 1.024744 | 0.990748 | 0.971026 | 1.011867 | 0.885729 | 0.948722 |

| 2024-09-11 00:00:00+00:00 | 1.024288 | 0.988299 | 0.980011 | 1.001351 | 0.896031 | 0.950876 |

| 2024-09-12 00:00:00+00:00 | 1.051865 | 1.011061 | 0.975672 | 0.987734 | 0.878328 | 0.940610 |

| 2024-09-13 00:00:00+00:00 | 1.061901 | 1.036981 | 0.987831 | 1.001874 | 0.885837 | 0.987858 |

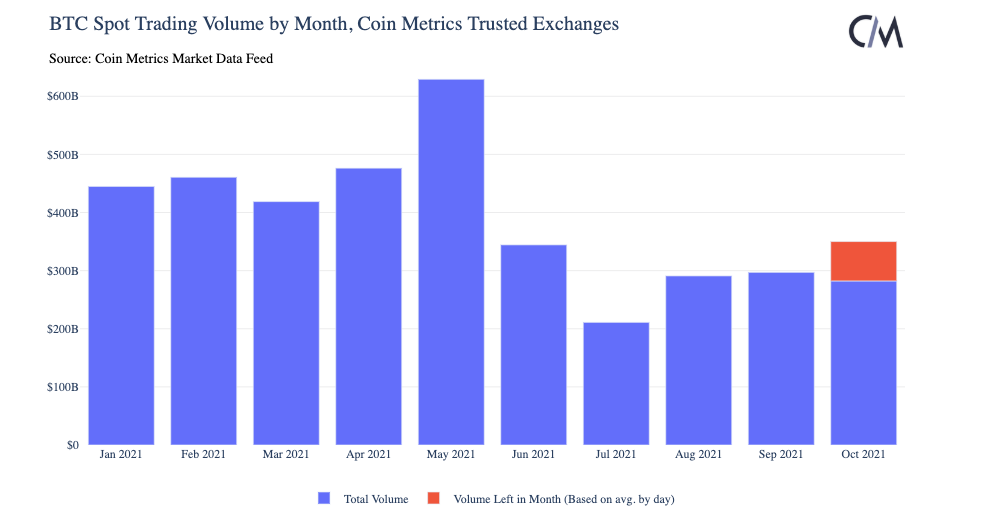

#### Example 2: Get daily spot trading volume on Coinbase for USDC markets

In [State of the Network #126](https://coinmetrics.substack.com/p/coin-metrics-state-of-the-network-issue-126), we looked at spot volume on trusted exchanges over time.

We can replicate similar data behind chart using just coinbase spot markets at 2021. Here, we derive volume from our `get_market_candles` endpoint.

```python

candles_coinbase = client.get_market_candles(

markets="coinbase-*-usdc-spot", # wildcards can be passed to get all asset pairs

start_time="2024-01-01",

end_time="2024-09-30",

frequency="1d"

).to_dataframe()

candles_coinbase["candle_usd_volume"] = candles_coinbase.candle_usd_volume.astype(float)

candles_coinbase["time"] = pd.to_datetime(candles_coinbase.time)

```

```

2024-10-25 15:23:45 INFO Sleeping for a rate limit window because 429 (too many requests) error was returned. Pleasesee Coin Metrics APIV4 documentation for more information: https://docs.coinmetrics.io/api/v4/#tag/Rate-limits

```

```python

candles_coinbase.head()

```

| | market | time | price\_open | price\_close | price\_high | price\_low | vwap | volume | candle\_usd\_volume | candle\_trades\_count |

| - | ----------------------- | ------------------------- | ----------- | ------------ | ----------- | ---------- | -------- | --------- | ------------------- | --------------------- |

| 0 | coinbase-eurc-usdc-spot | 2024-08-23 00:00:00+00:00 | 1.121 | 1.119 | 1.121 | 1.118 | 1.120121 | 997787.0 | 1.117636e+06 | 140 |

| 1 | coinbase-eurc-usdc-spot | 2024-08-24 00:00:00+00:00 | 1.12 | 1.12 | 1.13 | 1.119 | 1.120547 | 1122215.0 | 1.257359e+06 | 412 |

| 2 | coinbase-eurc-usdc-spot | 2024-08-25 00:00:00+00:00 | 1.121 | 1.12 | 1.132 | 1.119 | 1.121433 | 2796276.0 | 3.135467e+06 | 1727 |

| 3 | coinbase-eurc-usdc-spot | 2024-08-26 00:00:00+00:00 | 1.12 | 1.118 | 1.126 | 1.116 | 1.118883 | 1999004.0 | 2.236406e+06 | 882 |

| 4 | coinbase-eurc-usdc-spot | 2024-08-27 00:00:00+00:00 | 1.117 | 1.119 | 1.122 | 1.116 | 1.118849 | 1505368.0 | 1.684066e+06 | 1227 |

| | market | time | price\_open | price\_close | price\_high | price\_low | vwap | volume | candle\_usd\_volume | candle\_trades\_count |

| - | ----------------------- | ------------------------- | ----------- | ------------ | ----------- | ---------- | -------- | --------- | ------------------- | --------------------- |

| 0 | coinbase-eurc-usdc-spot | 2024-08-23 00:00:00+00:00 | 1.121 | 1.119 | 1.121 | 1.118 | 1.120121 | 997787.0 | 1.117636e+06 | 140 |

| 1 | coinbase-eurc-usdc-spot | 2024-08-24 00:00:00+00:00 | 1.12 | 1.12 | 1.13 | 1.119 | 1.120547 | 1122215.0 | 1.257357e+06 | 412 |

| 2 | coinbase-eurc-usdc-spot | 2024-08-25 00:00:00+00:00 | 1.121 | 1.12 | 1.132 | 1.119 | 1.121433 | 2796276.0 | 3.135472e+06 | 1727 |

| 3 | coinbase-eurc-usdc-spot | 2024-08-26 00:00:00+00:00 | 1.12 | 1.118 | 1.126 | 1.116 | 1.118883 | 1999004.0 | 2.236419e+06 | 882 |

| 4 | coinbase-eurc-usdc-spot | 2024-08-27 00:00:00+00:00 | 1.117 | 1.119 | 1.122 | 1.116 | 1.118849 | 1505368.0 | 1.684074e+06 | 1227 |

We can also break this down by month. Note that for this example, the volume numbers will look smaller because we are using fewer exchanges.

```python

month_order = [

'January', 'February', 'March', 'April', 'May', 'June',

'July', 'August', 'September', 'October', 'November', 'December'

]

candles_coinbase.groupby(

candles_coinbase.time.dt.month_name()

)[['candle_usd_volume']].sum().reindex(month_order).dropna()

```

| | candle\_usd\_volume |

| --------- | ------------------- |

| time | |

| January | 4.401994e+08 |

| February | 1.227417e+08 |

| March | 2.522828e+08 |

| April | 1.476761e+08 |

| May | 2.575348e+08 |

| June | 9.312749e+08 |

| July | 1.331209e+09 |

| August | 2.433962e+09 |

| September | 1.849214e+09 |

---

# Agent Instructions

This documentation is published with GitBook. GitBook is the documentation platform designed so that both humans and AI agents can read, navigate, and reason over technical content effectively. Learn more at gitbook.com.

## Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter, and the optional `goal` query parameter:

```

GET https://gitbook-docs.coinmetrics.io/tutorials-and-examples/tutorials/walkthrough_community.md?ask=&goal=

```

`ask` is the immediate question: it should be specific, self-contained, and written in natural language.

`goal` is optional and describes the broader end goal you are ultimately trying to accomplish on behalf of the user. GitBook uses it to tailor the answer towards what is most useful for that goal.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.

Coin Metrics supports several metrics for various data types such as exchanges, markets, and asset-pairs.

You can also bound your queries by using the `limit` parameter.

```python

df_asset_metrics_limit = client.get_asset_metrics(

assets=assets,

metrics=btc_metrics[:5],

start_time=start_time,

end_time=end_time,

limit_per_asset=2

).to_dataframe()

```

```python

df_asset_metrics_limit

```

| | asset | time | AdrActCnt | AdrBal1in100KCnt | AdrBal1in100MCnt | AdrBal1in10BCnt | AdrBal1in10KCnt |

| - | ----- | ------------------------- | --------- | ---------------- | ---------------- | --------------- | --------------- |

| 0 | btc | 2024-09-01 00:00:00+00:00 | 660770 | 9283 | 3046587 | 20365534 | 973 |

| 1 | btc | 2024-09-02 00:00:00+00:00 | 717673 | 9284 | 3046904 | 20359814 | 972 |

| 2 | eth | 2024-09-01 00:00:00+00:00 | 548611 | 6907 | 1836310 | 27996184 | 1221 |

| 3 | eth | 2024-09-02 00:00:00+00:00 | 488354 | 6902 | 1836617 | 28008369 | 1218 |

| | asset | time | AdrActCnt | AdrBal1in100KCnt | AdrBal1in100MCnt | AdrBal1in10BCnt | AdrBal1in10KCnt |

| - | ----- | ------------------------- | --------- | ---------------- | ---------------- | --------------- | --------------- |

| 0 | btc | 2024-08-15 00:00:00+00:00 | 715632 | 9229 | 3054724 | 20292616 | 973 |

| 1 | btc | 2024-08-16 00:00:00+00:00 | 700335 | 9231 | 3055010 | 20300505 | 977 |

| 2 | eth | 2024-08-15 00:00:00+00:00 | 603353 | 6862 | 1837926 | 27972812 | 1226 |

| 3 | eth | 2024-08-16 00:00:00+00:00 | 541263 | 6871 | 1837366 | 27962507 | 1223 |

#### Market Observations

The other common timeseries data type that you will encounter are individual observations.

First, we will need to familiarize ourselves with the market convention which we can find on faqs. You can see a full list of markets by using the `reference-data` endpoint.

```python

df_coinbase_btc_markets = client.reference_data_markets(asset='btc', exchange='coinbase').to_dataframe()

```

```python

df_coinbase_btc_markets.head()

```

| | market | exchange | base | quote | pair | symbol | type | size\_asset | margin\_asset | strike | ... | order\_price\_increment | order\_price\_min | order\_price\_max | order\_size\_min | order\_taker\_fee | order\_maker\_fee | margin\_trading\_enabled | experimental | base\_native | quote\_native |

| - | ----------------------- | -------- | ----- | ----- | --------- | --------- | ---- | ----------- | ------------- | ------ | --- | ----------------------- | ----------------- | ----------------- | ---------------- | ----------------- | ----------------- | ------------------------ | ------------ | ------------ | ------------- |

| 0 | coinbase-1inch-btc-spot | coinbase | 1inch | btc | 1inch-btc | 1INCH-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 1 | coinbase-aave-btc-spot | coinbase | aave | btc | aave-btc | AAVE-BTC | spot | \ | \ | \ | ... | 0.000001 | 0.000001 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 2 | coinbase-ada-btc-spot | coinbase | ada | btc | ada-btc | ADA-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 3 | coinbase-algo-btc-spot | coinbase | algo | btc | algo-btc | ALGO-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

| 4 | coinbase-ankr-btc-spot | coinbase | ankr | btc | ankr-btc | ANKR-BTC | spot | \ | \ | \ | ... | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ | \ | \ |

5 rows × 39 columns

| | market | exchange | base | quote | pair | symbol | type | size\_asset | margin\_asset | strike | ... | order\_amount\_min | order\_amount\_max | order\_price\_increment | order\_price\_min | order\_price\_max | order\_size\_min | order\_taker\_fee | order\_maker\_fee | margin\_trading\_enabled | experimental |

| - | ----------------------- | -------- | ----- | ----- | --------- | --------- | ---- | ----------- | ------------- | ------ | --- | ------------------ | ------------------ | ----------------------- | ----------------- | ----------------- | ---------------- | ----------------- | ----------------- | ------------------------ | ------------ |

| 0 | coinbase-1inch-btc-spot | coinbase | 1inch | btc | 1inch-btc | 1INCH-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

| 1 | coinbase-aave-btc-spot | coinbase | aave | btc | aave-btc | AAVE-BTC | spot | \ | \ | \ | ... | \ | \ | 0.000001 | 0.000001 | \ | 0.000016 | \ | \ | False | \ |

| 2 | coinbase-ada-btc-spot | coinbase | ada | btc | ada-btc | ADA-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

| 3 | coinbase-algo-btc-spot | coinbase | algo | btc | algo-btc | ALGO-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

| 4 | coinbase-ankr-btc-spot | coinbase | ankr | btc | ankr-btc | ANKR-BTC | spot | \ | \ | \ | ... | \ | \ | 0.0 | 0.0 | \ | 0.000016 | \ | \ | False | \ |

5 rows × 37 columns

We can then pass these markets onto the `timeseries/market-*` endpoints. Below is an example of how to pull individual market trades.

```python

df_coinbase_btc_trades = client.get_market_trades(

markets=["coinbase-btc-usd-spot"],

start_time=datetime.now()-timedelta(seconds=60),

end_time=datetime.now(),

).to_dataframe()

```

```python

df_coinbase_btc_trades.head()

```

| | market | time | coin\_metrics\_id | amount | price | database\_time | side |

| - | --------------------- | -------------------------------- | ----------------- | -------- | -------- | -------------------------------- | ---- |

| 0 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966854 | 0.000004 | 68353.27 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 1 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966855 | 0.000012 | 68353.27 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 2 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966856 | 0.002187 | 68354.37 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 3 | coinbase-btc-usd-spot | 2024-10-25 15:22:44.919441+00:00 | 705966857 | 0.002523 | 68354.38 | 2024-10-25 15:22:45.721609+00:00 | buy |

| 4 | coinbase-btc-usd-spot | 2024-10-25 15:22:45.078614+00:00 | 705966858 | 0.001043 | 68353.27 | 2024-10-25 15:22:45.721609+00:00 | buy |

| | market | time | coin\_metrics\_id | amount | price | database\_time | side |

| - | --------------------- | -------------------------------- | ----------------- | -------- | -------- | -------------------------------- | ---- |

| 0 | coinbase-btc-usd-spot | 2024-09-13 16:55:02.663733+00:00 | 691698441 | 0.008 | 59491.6 | 2024-09-13 16:55:03.253369+00:00 | sell |

| 1 | coinbase-btc-usd-spot | 2024-09-13 16:55:02.670644+00:00 | 691698442 | 0.008 | 59491.61 | 2024-09-13 16:55:03.253369+00:00 | buy |

| 2 | coinbase-btc-usd-spot | 2024-09-13 16:55:03.057923+00:00 | 691698443 | 0.001186 | 59491.61 | 2024-09-13 16:55:03.771512+00:00 | buy |

| 3 | coinbase-btc-usd-spot | 2024-09-13 16:55:03.143752+00:00 | 691698444 | 0.15742 | 59491.6 | 2024-09-13 16:55:03.771512+00:00 | sell |

| 4 | coinbase-btc-usd-spot | 2024-09-13 16:55:03.143816+00:00 | 691698445 | 0.076281 | 59491.6 | 2024-09-13 16:55:03.771512+00:00 | sell |

#### Examples from State of the Network

The Python API Client is often used for transforming data for [State of the Network](https://coinmetrics.substack.com/). Below are some examples of data transformations done to produce the data visualizations.

**Example 1: Get returns by coin in the CM reference rates universe over the last 10-years**

In [State of the Network #128](https://coinmetrics.substack.com/p/coin-metrics-state-of-the-network-53b), we looked at the returns for each asset dating back the last 10 years.

We can generate this data by weaving in the `catalog_asset_metrics_v2` and `get_asset_metrics` endpoint. The code snippets below demonstrate how to do this with a small list of assets.

```python

# Get all assets that have a reference rate

assets_refrate = client.catalog_asset_metrics_v2(metrics="ReferenceRateUSD")

# Get list of assets with daily ref rate

# uncomment the top line to look at *every* asset with reference rates

# asset_with_ref_rates = assets_refrate[0]["frequencies"][0]["assets"]

asset_with_ref_rates = ['btc', 'eth', 'bnb', 'ada', 'doge', 'xrp']

#Query API for prices, daily CM reference rates as dataframe

metrics = "ReferenceRateUSD"

frequency = "1d"

logging.info("Getting prices...")

df_prices = client.get_asset_metrics(

assets=asset_with_ref_rates,

metrics=metrics,

frequency=frequency,

start_time=start_time,

end_time=end_time

).to_dataframe()

# Assign datatypes

df_prices["time"] = pd.to_datetime(df_prices.time)

df_prices["ReferenceRateUSD"] = df_prices.ReferenceRateUSD.astype(float)

# Reshape dataset so assets are in columns, dates are the rows, and the values are prices

df_prices_pivot = df_prices.pivot(

index="time",

columns="asset",

values="ReferenceRateUSD"

)

# Index each asset's time series to 1

for col in df_prices_pivot.columns:

logging.info(f"Calculating Reference rate for {col}....")

# First price in time series

first_price = df_prices_pivot[df_prices_pivot[col].notnull()][col].iloc[0]

# Index time series

df_prices_pivot[col] = df_prices_pivot[col]/first_price

# Fill forward for Null values

df_prices_pivot[col] = df_prices_pivot[col].ffill()

```

```

2024-10-25 15:23:44 INFO Getting prices...

2024-10-25 15:23:45 INFO Calculating Reference rate for ada....

2024-10-25 15:23:45 INFO Calculating Reference rate for bnb....

2024-10-25 15:23:45 INFO Calculating Reference rate for btc....

2024-10-25 15:23:45 INFO Calculating Reference rate for doge....

2024-10-25 15:23:45 INFO Calculating Reference rate for eth....

2024-10-25 15:23:45 INFO Calculating Reference rate for xrp....

```

```

2024-09-13 16:56:10 INFO Getting prices...

2024-09-13 16:56:11 INFO Calculating Reference rate for ada....

2024-09-13 16:56:11 INFO Calculating Reference rate for bnb....

2024-09-13 16:56:11 INFO Calculating Reference rate for btc....

2024-09-13 16:56:11 INFO Calculating Reference rate for doge....

2024-09-13 16:56:11 INFO Calculating Reference rate for eth....

2024-09-13 16:56:11 INFO Calculating Reference rate for xrp....

```

```python

df_prices_pivot.tail()

```

| asset | ada | bnb | btc | doge | eth | xrp |

| ------------------------- | -------- | -------- | -------- | -------- | -------- | -------- |

| time | | | | | | |

| 2024-09-26 00:00:00+00:00 | 1.102137 | 1.100617 | 1.069534 | 1.070347 | 1.024427 | 1.030510 |

| 2024-09-27 00:00:00+00:00 | 1.162204 | 1.118540 | 1.103424 | 1.164025 | 1.046276 | 1.042040 |

| 2024-09-28 00:00:00+00:00 | 1.165724 | 1.141772 | 1.115465 | 1.222446 | 1.073526 | 1.040046 |

| 2024-09-29 00:00:00+00:00 | 1.158667 | 1.127693 | 1.115512 | 1.267128 | 1.064176 | 1.084632 |

| 2024-09-30 00:00:00+00:00 | 1.151477 | 1.119118 | 1.112921 | 1.232789 | 1.056856 | 1.133519 |

| asset | ada | bnb | btc | doge | eth | xrp |

| ------------------------- | -------- | -------- | -------- | -------- | -------- | -------- |

| time | | | | | | |

| 2024-09-09 00:00:00+00:00 | 1.008826 | 0.960197 | 0.932336 | 0.936040 | 0.862489 | 0.930312 |

| 2024-09-10 00:00:00+00:00 | 1.024744 | 0.990748 | 0.971026 | 1.011867 | 0.885729 | 0.948722 |

| 2024-09-11 00:00:00+00:00 | 1.024288 | 0.988299 | 0.980011 | 1.001351 | 0.896031 | 0.950876 |

| 2024-09-12 00:00:00+00:00 | 1.051865 | 1.011061 | 0.975672 | 0.987734 | 0.878328 | 0.940610 |

| 2024-09-13 00:00:00+00:00 | 1.061901 | 1.036981 | 0.987831 | 1.001874 | 0.885837 | 0.987858 |

#### Example 2: Get daily spot trading volume on Coinbase for USDC markets

In [State of the Network #126](https://coinmetrics.substack.com/p/coin-metrics-state-of-the-network-issue-126), we looked at spot volume on trusted exchanges over time.

We can replicate similar data behind chart using just coinbase spot markets at 2021. Here, we derive volume from our `get_market_candles` endpoint.

```python

candles_coinbase = client.get_market_candles(

markets="coinbase-*-usdc-spot", # wildcards can be passed to get all asset pairs

start_time="2024-01-01",

end_time="2024-09-30",

frequency="1d"

).to_dataframe()

candles_coinbase["candle_usd_volume"] = candles_coinbase.candle_usd_volume.astype(float)

candles_coinbase["time"] = pd.to_datetime(candles_coinbase.time)

```

```

2024-10-25 15:23:45 INFO Sleeping for a rate limit window because 429 (too many requests) error was returned. Pleasesee Coin Metrics APIV4 documentation for more information: https://docs.coinmetrics.io/api/v4/#tag/Rate-limits

```

```python

candles_coinbase.head()

```

| | market | time | price\_open | price\_close | price\_high | price\_low | vwap | volume | candle\_usd\_volume | candle\_trades\_count |

| - | ----------------------- | ------------------------- | ----------- | ------------ | ----------- | ---------- | -------- | --------- | ------------------- | --------------------- |

| 0 | coinbase-eurc-usdc-spot | 2024-08-23 00:00:00+00:00 | 1.121 | 1.119 | 1.121 | 1.118 | 1.120121 | 997787.0 | 1.117636e+06 | 140 |

| 1 | coinbase-eurc-usdc-spot | 2024-08-24 00:00:00+00:00 | 1.12 | 1.12 | 1.13 | 1.119 | 1.120547 | 1122215.0 | 1.257359e+06 | 412 |

| 2 | coinbase-eurc-usdc-spot | 2024-08-25 00:00:00+00:00 | 1.121 | 1.12 | 1.132 | 1.119 | 1.121433 | 2796276.0 | 3.135467e+06 | 1727 |

| 3 | coinbase-eurc-usdc-spot | 2024-08-26 00:00:00+00:00 | 1.12 | 1.118 | 1.126 | 1.116 | 1.118883 | 1999004.0 | 2.236406e+06 | 882 |

| 4 | coinbase-eurc-usdc-spot | 2024-08-27 00:00:00+00:00 | 1.117 | 1.119 | 1.122 | 1.116 | 1.118849 | 1505368.0 | 1.684066e+06 | 1227 |

| | market | time | price\_open | price\_close | price\_high | price\_low | vwap | volume | candle\_usd\_volume | candle\_trades\_count |

| - | ----------------------- | ------------------------- | ----------- | ------------ | ----------- | ---------- | -------- | --------- | ------------------- | --------------------- |

| 0 | coinbase-eurc-usdc-spot | 2024-08-23 00:00:00+00:00 | 1.121 | 1.119 | 1.121 | 1.118 | 1.120121 | 997787.0 | 1.117636e+06 | 140 |

| 1 | coinbase-eurc-usdc-spot | 2024-08-24 00:00:00+00:00 | 1.12 | 1.12 | 1.13 | 1.119 | 1.120547 | 1122215.0 | 1.257357e+06 | 412 |

| 2 | coinbase-eurc-usdc-spot | 2024-08-25 00:00:00+00:00 | 1.121 | 1.12 | 1.132 | 1.119 | 1.121433 | 2796276.0 | 3.135472e+06 | 1727 |

| 3 | coinbase-eurc-usdc-spot | 2024-08-26 00:00:00+00:00 | 1.12 | 1.118 | 1.126 | 1.116 | 1.118883 | 1999004.0 | 2.236419e+06 | 882 |

| 4 | coinbase-eurc-usdc-spot | 2024-08-27 00:00:00+00:00 | 1.117 | 1.119 | 1.122 | 1.116 | 1.118849 | 1505368.0 | 1.684074e+06 | 1227 |

We can also break this down by month. Note that for this example, the volume numbers will look smaller because we are using fewer exchanges.

```python

month_order = [

'January', 'February', 'March', 'April', 'May', 'June',

'July', 'August', 'September', 'October', 'November', 'December'

]

candles_coinbase.groupby(

candles_coinbase.time.dt.month_name()

)[['candle_usd_volume']].sum().reindex(month_order).dropna()

```

| | candle\_usd\_volume |

| --------- | ------------------- |

| time | |

| January | 4.401994e+08 |

| February | 1.227417e+08 |

| March | 2.522828e+08 |

| April | 1.476761e+08 |

| May | 2.575348e+08 |

| June | 9.312749e+08 |

| July | 1.331209e+09 |

| August | 2.433962e+09 |

| September | 1.849214e+09 |

---

# Agent Instructions

This documentation is published with GitBook. GitBook is the documentation platform designed so that both humans and AI agents can read, navigate, and reason over technical content effectively. Learn more at gitbook.com.

## Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter, and the optional `goal` query parameter:

```

GET https://gitbook-docs.coinmetrics.io/tutorials-and-examples/tutorials/walkthrough_community.md?ask=&goal=

```

`ask` is the immediate question: it should be specific, self-contained, and written in natural language.

`goal` is optional and describes the broader end goal you are ultimately trying to accomplish on behalf of the user. GitBook uses it to tailor the answer towards what is most useful for that goal.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.